Bad credit can hold you back from a lot of things, and it becomes an even bigger issue with small business loans. To the lenders, having poor credit makes you look like a high-risk client, which is the kind of situation most banks typically try to avoid. Fortunately, there are still a couple of ways you can get a business loan, even if you have a low credit score.

One of the first ways to secure a business loan is by taking advantage of the Small Business Association's (SBA) 7(a) loans. These loans are government-guaranteed, which lowers the risk for the SBA. You can get a list from the SBA of lenders who would be more than happy to take a look at your situation. Be sure to speak with an SBA agent before presenting your request to a bank to ensure success.

A second way to get a business loan with bad credit is by offering up collateral. Collateral can include your home, equipment, other businesses, or land. By providing insurance, you’re lowering the risk of loss for the lender, making them much more likely to accept you. The more you offer, the better off you’ll be.

Understanding Credit Scores and Their Impact

Before diving into how to secure a business loan with bad credit, it’s essential to understand what credit scores are and why they matter. A credit score is a numerical representation of your creditworthiness based on your credit history. Lenders use this score to evaluate the risk of lending money to you.

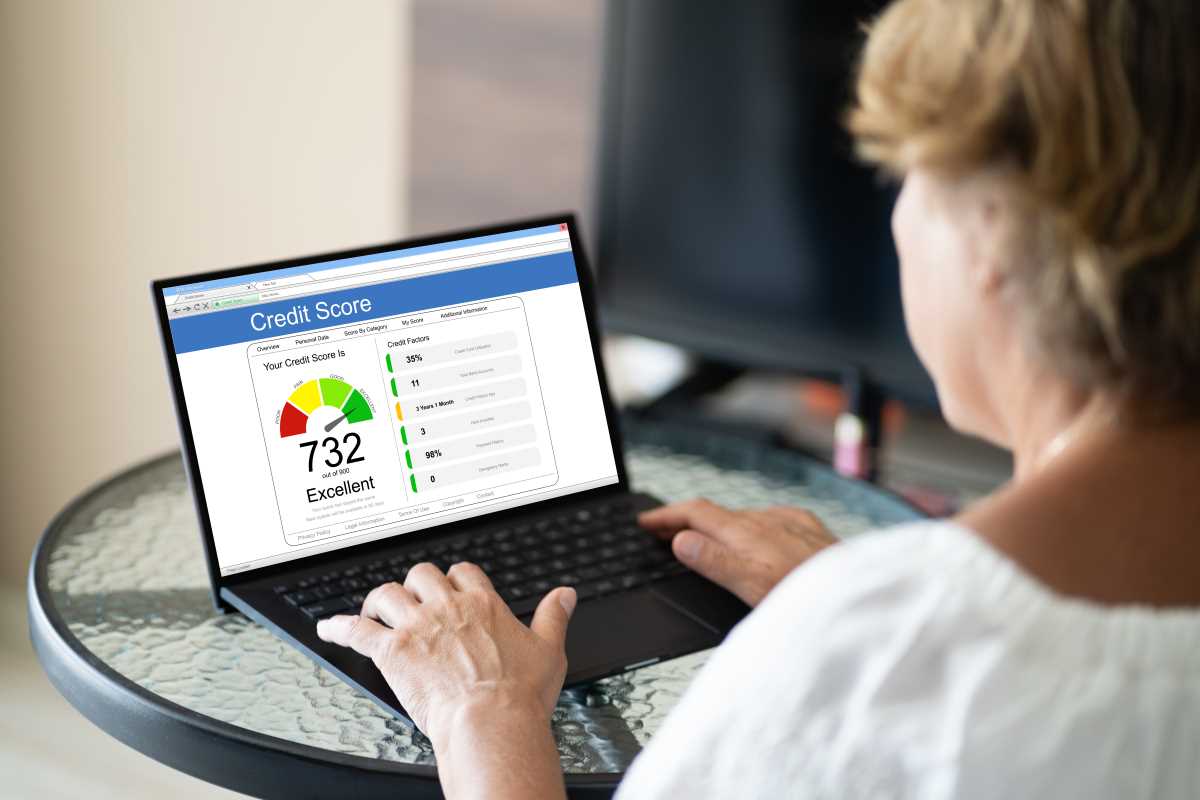

Scores typically range from 300 to 850, with higher scores indicating better creditworthiness. A score below 580 is generally considered bad credit, and a score between 580 and 669 is considered fair.

Credit scores are crucial in the lending process because they provide a quick and standardized way for lenders to assess how likely you are to repay a loan. A low score can signal to lenders that you might be a higher risk, which could result in higher interest rates, stricter loan terms, or outright denial of your loan application.

Understand Your Credit Profile

Before applying for a business loan, it's crucial to understand your credit profile. Obtain a copy of your credit report and review it for any inaccuracies or outdated information. You can dispute any errors with the credit bureaus to ensure your credit report reflects your current financial situation.

Additionally, familiarize yourself with your credit score, which is a key factor lenders use to evaluate loan applications. Knowing your credit score will help you identify which loan options are more likely to be available to you.

Improve Your Credit Score

While it may not be a quick fix, taking steps to improve your credit score can enhance your chances of securing a loan. Start by paying down outstanding debts, making timely payments, and reducing your credit utilization ratio.

Avoid taking on new debt or applying for multiple credit lines, as these actions can negatively impact your credit score. Over time, improving your credit profile will not only increase your chances of getting a loan but also help you secure better interest rates and terms.

Build Relationships with Lenders

Building a strong relationship with potential lenders can be beneficial, especially if you have bad credit. Regularly communicate with lenders, keep them informed about your business progress, and demonstrate your commitment to improving your financial situation.

A positive relationship with lenders can enhance your credibility and increase the likelihood of securing financing in the future.

Look for Government-Backed Loans

Government-backed loan programs, such as those offered by the Small Business Administration (SBA), may be available to businesses with bad credit. These programs are designed to support small businesses by providing guarantees to lenders, reducing their risk.

While government-backed loans may still have credit requirements, they can be more accessible than traditional loans. Research SBA loan programs and other government-backed financing options to see if you qualify.

Challenges of Securing a Business Loan with Bad Credit

When you have bad credit, several challenges can arise when trying to secure a business loan:

Limited Loan Options

Traditional lenders, such as banks and credit unions, often have stringent credit score requirements. If your score is below a certain threshold, you might not qualify for their loans, limiting your options to alternative lenders, which may have higher costs.

Higher Interest Rates

If you do qualify for a loan, expect to pay a higher interest rate. Lenders compensate for the increased risk associated with bad credit by charging more for the loan. This can make the loan more expensive over time.

Shorter Loan Terms

If you find a lender willing to work with you despite your bad credit, be prepared to negotiate the loan terms. Interest rates, repayment periods, and fees can often be adjusted based on your needs and the lender’s assessment of your situation.

Be transparent about your credit history and financial situation, and work with the lender to find manageable terms for your business.

Collateral Requirements

Lenders might require collateral to secure the loan. This means putting up assets such as real estate, equipment, or inventory that the lender can seize if you default on the loan.

Personal Guarantees

If you have bad credit, a co-signer or guarantor with a strong credit history can enhance your loan application. A co-signer agrees to take on the responsibility of repaying the loan if you default, which reduces the lender’s risk.

Similarly, a guarantor provides a personal guarantee to cover the loan if you are unable to repay it. Having a co-signer or guarantor can increase your chances of approval and may help you secure better loan terms.

Explore Microloans

Microloans are small loans designed to help small businesses and startups that may not qualify for traditional financing. Nonprofit organizations or community lenders often offer these loans and may have more lenient credit requirements.

Microloans can provide the necessary capital for businesses in their early stages or those with limited credit histories. Research local microloan programs or organizations that offer microloans to see if you qualify.